Blockchain Explained

May 12, 2022

What Is a Blockchain?

A blockchain is a digital database shared among computer nodes. Blockchain’s innovation generates trust without requiring a third party and collects data in blocks that contain data sets. Blockchains are best known for their crucial role in cryptocurrency systems, such as Bitcoin, for maintaining a secure and decentralized record of transactions. The innovation of a blockchain is that it guarantees the fidelity and security of a record of data and generates trust without the need for a trusted third party.

The data structure of a blockchain differs from a traditional database. A blockchain collects data in blocks that contain data sets. In the blockchain, blocks are linked together to form a data chain known as a blockchain. All subsequent information is compiled into a new block, then added to the chain.

A database usually structures its data into tables, whereas a blockchain, as its name implies, structures its data into chunks (blocks) that are strung together. This data structure inherently makes an irreversible timeline of data when implemented in a decentralized nature. When a block is filled, it is set in stone and becomes a part of this timeline. Each block in the chain is given an exact timestamp when added to the chain.

How Does a Blockchain Work?

The goal of blockchain is to record and distribute digital data without editing it. A blockchain thus supports immutable ledgers, or records of transactions that cannot be altered, deleted, or destroyed. This is why blockchains are called distributed ledger technology (DLT).

The blockchain concept was first proposed in 1991 as a research project, before its first widespread use in 2009: Bitcoin. Since then, blockchains have been used to create cryptocurrencies, decentralized finance (DeFi) applications, non-fungible tokens (NFTs), and smart contracts.

Transaction Process.

![]()

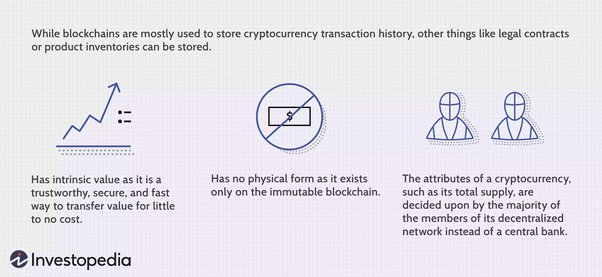

Attributes of Cryptocurrency

(Source: Investopedia)

Blockchain Decentralization

Imagine that a company owns a server farm with 10,000 computers used to maintain a database holding all of its client’s account information. In addition, this company owns a warehouse building that contains all of these computers under one roof and has full control of each of these computers and all of the information contained within them. This, however, provides a single point of failure. What happens if the electricity at that location goes out? What if its Internet connection is severed? What if it burns to the ground? What if a bad actor erases everything with a single keystroke? In any case, the data is lost or corrupted.

A blockchain allows data to be spread across multiple network nodes located worldwide. So, if someone tries to change a record at one node of the database, the other nodes will not be altered, preventing a bad actor from doing so. For example, if one user tampers with Bitcoin’s transaction record, all other nodes can easily cross-reference and find the offending node. This system helps establish a precise and transparent timeline. Thus, no node within the network can alter data held within it.

Because of this, the information and history (such as transactions of a cryptocurrency) are irreversible. Such a record could be a list of transactions (such as with a cryptocurrency). Still, it also is possible for a blockchain to hold a variety of other information like legal contracts, state identifications, or a company’s product inventory.

Transparency

Because Bitcoin’s blockchain is decentralized, anyone can see all transactions by running a personal node or using blockchain explorers. Each node keeps its own copy of the chain, which is updated as new blocks are added. So you could track Bitcoin anywhere if you wanted to.

For example, exchanges have been hacked before, and those who kept Bitcoin on the exchange lost everything. Even if the hacker is completely unknown, the Bitcoins they stole are easy to track down. If the Bitcoins that were stolen in some of these hacks were moved or spent somewhere, it would be known.

The records that are kept in the Bitcoin blockchain, as well as in most other places, are, of course, encrypted. This means that only the record’s owner can decrypt it to find out who it belongs to (using a public-private key pair). So, people who use blockchains can stay anonymous while still keeping things open.

Is Blockchain Secure?

Blockchain technology can provide decentralized security and trust in several ways. First of all, new blocks are always put in order and in a straight line. That is, they are always added to the “end” of the chain. Once a block has been added to the end of the blockchain, it is difficult to change its contents without the majority of the network agrees. This is because each block has its own hash, as well as the hash of the block before it and the time stamp that we already talked about. A mathematical function converts digital data into numbers and letters. If any of this data changes, the hash code changes.

Let’s say a hacker who also runs a node on a blockchain network wants to change a blockchain and steal cryptocurrency from everyone else. If they changed their own single copy, it wouldn’t match the copies of everyone else. When everyone else compares their copies to each other, this one copy would stand out, and that hacker’s version of the chain would be thrown out as fake.

For this hack to work, the hacker would have to control and change 51% or more of the copies of the blockchain at the same time, making their copy the majority copy and the agreed-upon chain. Such an attack would also cost a lot of money and time because all of the blocks would have to be redone because their timestamps and hash codes would be different.

Due to the rapid growth of many cryptocurrency networks, this would be ridiculously expensive and also unlikely to work. This wouldn’t go unnoticed because the network would notice the big changes to the blockchain. Members of the network would then hard fork to an unaffected chain. The attacker would then be in control of a worthless asset, rendering the attack futile. The same would happen if the bad guy attacked the new Bitcoin fork. It is set up so that joining the network is far more profitable than attacking it.

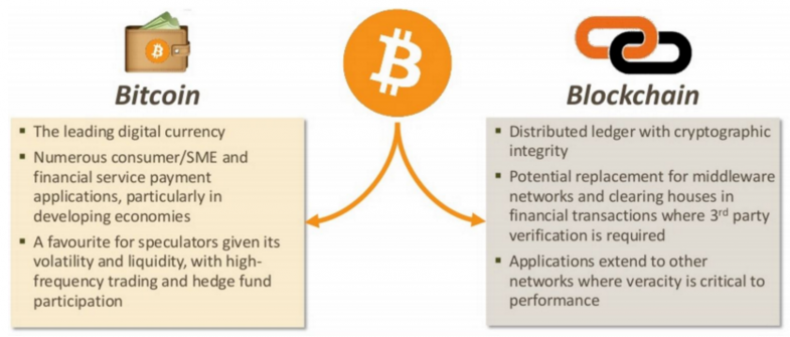

Bitcoin vs. Blockchain

In 1991, Stuart Haber and W. Scott Stornetta, two researchers, came up with the idea for blockchain technology. They wanted to set up a system where document timestamps could not be changed. But blockchain didn’t have its first real-world use until almost 20 years later, when Bitcoin came out in January 2009.

A blockchain is the foundation of the Bitcoin protocol. Satoshi Nakamoto, who created Bitcoin under a fake name, wrote about it in a research paper as “a new electronic cash system that is fully peer-to-peer, with no trusted third party.”

The most important thing to know is that Bitcoin only uses blockchain to record a transparent ledger of payments. However, blockchain could be used to record any number of data points in a way that can’t be changed. As we’ve already talked about, this could include transactions, votes in an election, inventories of goods, state IDs, home deeds, and much more.

At the moment, tens of thousands of projects are looking for ways to use blockchains to help society in ways other than just recording transactions. For example, blockchains could be used to make voting in democratic elections more secure. Because blockchain can’t be changed, it would be much harder for people to vote more than once. For example, each citizen of a country could be given one cryptocurrency or token as part of the voting process. Then, each candidate would be given a unique wallet address, and voters would send their token or cryptocurrency to the address of the candidate they want to vote for. Because blockchain is transparent and easy to track, it would eliminate the need for humans to count votes and the ability of bad people to change physical ballots.

How Are Blockchains Used?

As we now know, Bitcoin’s blockchain stores information about money transactions in blocks. On the blockchain, there are now more than 10,000 other cryptocurrency systems. But it turns out that blockchain is also a good way to store information about other kinds of transactions.

Some companies that have already incorporated blockchain include Walmart, Pfizer, AIG, Siemens, Unilever, and a host of others. For example, IBM has created its Food Trust blockchain to trace the journey that food products take to get to their locations.

Why do that? There have been many outbreaks of E. coli, salmonella, and listeria in the food industry, as well as accidents where dangerous materials got into food. In the past, it took weeks to figure out where these outbreaks came from or what people were eating that made them sick. Using blockchain, brands can track where a food item comes from, where it stops along the way, and where it finally ends up. If a food is found to be tainted, it can be traced back through each stop to where it came from. Not only that, but these companies can now also see everything else they may have come in contact with. This means that the problem can be found much faster, which could save lives. This is one way that blockchain is used in the real world, but there are many other ways as well.

Banking and Finance

Banks may be the industry that stands to benefit the most from using blockchain. Financial institutions only work from 9 am to 5 pm, five days a week. So, if you deposit a check at 6 p.m. on Friday, the funds may not appear in your account until Monday. A deposit made during business hours can take one to three days to be verified as banks have many transactions to settle. On the contrary, blockchain is always working.

By adding blockchain to banks, customers’ transactions can be processed in as little as 10 minutes, which is about how long it takes to add a block to the blockchain, no matter what day of the week it is or what holiday it is. With blockchain, banks will also be able to move money more quickly and safely between institutions. In the stock trading business, for example, the settlement and clearing process can take up to three days (or longer if trading internationally), during which time the money and shares are frozen.

Given the size of the sums involved, even the few days that the money is in transit can carry significant costs and risks for banks.

Currency

Coins like Bitcoin use blockchain. The Fed controls the US dollar. A user’s data and money are technically at the mercy of their bank or government. If a user’s bank is hacked, their personal data is exposed. The value of the client’s currency may be at risk if their bank fails or if their government is unstable. In 2008, taxpayers saved several failing banks. These concerns prompted the creation of Bitcoin.

Blockchain allows Bitcoin and other cryptocurrencies to operate decentralized. It does this by spreading its operations across a network of computers. This lowers the risk and gets rid of a lot of the fees for processing and transactions. This reduces risk and eliminates many transaction fees. In addition, a more stable currency that can be used in more places and with more people and institutions can help people in countries with unstable currencies or weak financial systems.

Those who don’t have state identification can save money in cryptocurrency wallets or use them to pay for things. Some countries may be in the middle of a war or have governments that lack the infrastructure to give people IDs. People in these countries may not have access to savings accounts or brokerage accounts, which means they have no safe way to store their money.

Healthcare

Blockchain can help healthcare providers store the medical records of their patients in a safe way. When a medical record is made and signed, it can be added to the blockchain. This gives patients proof that the record can’t be changed. With a private key, these health records could be encrypted and stored on the blockchain so that only certain people could access them. This would protect their privacy.

Property Records

If you’ve ever been to your town’s Recorder’s Office, you know that recording property rights is a time-consuming and inefficient process. Today, a physical deed must be given to a government employee at the local recording office, where it is entered by hand into the county’s central database and public index. In the case of a property dispute, claims to the property must be matched with the public index.

And it’s not just expensive and time-consuming. Human tends to make mistakes and as a result, makes it harder to track who owns what. Cryptocurrency may eliminate the need to scan documents and search local records. Property owners can rest assured that their deed is correct and will always be there if stored and checked on the blockchain.

It’s difficult to prove ownership of property in war-torn countries or areas with limited government or financial infrastructure, let alone a Recorder’s Office. A group of people living in such a place could use blockchain to establish clear and transparent property ownership timelines.

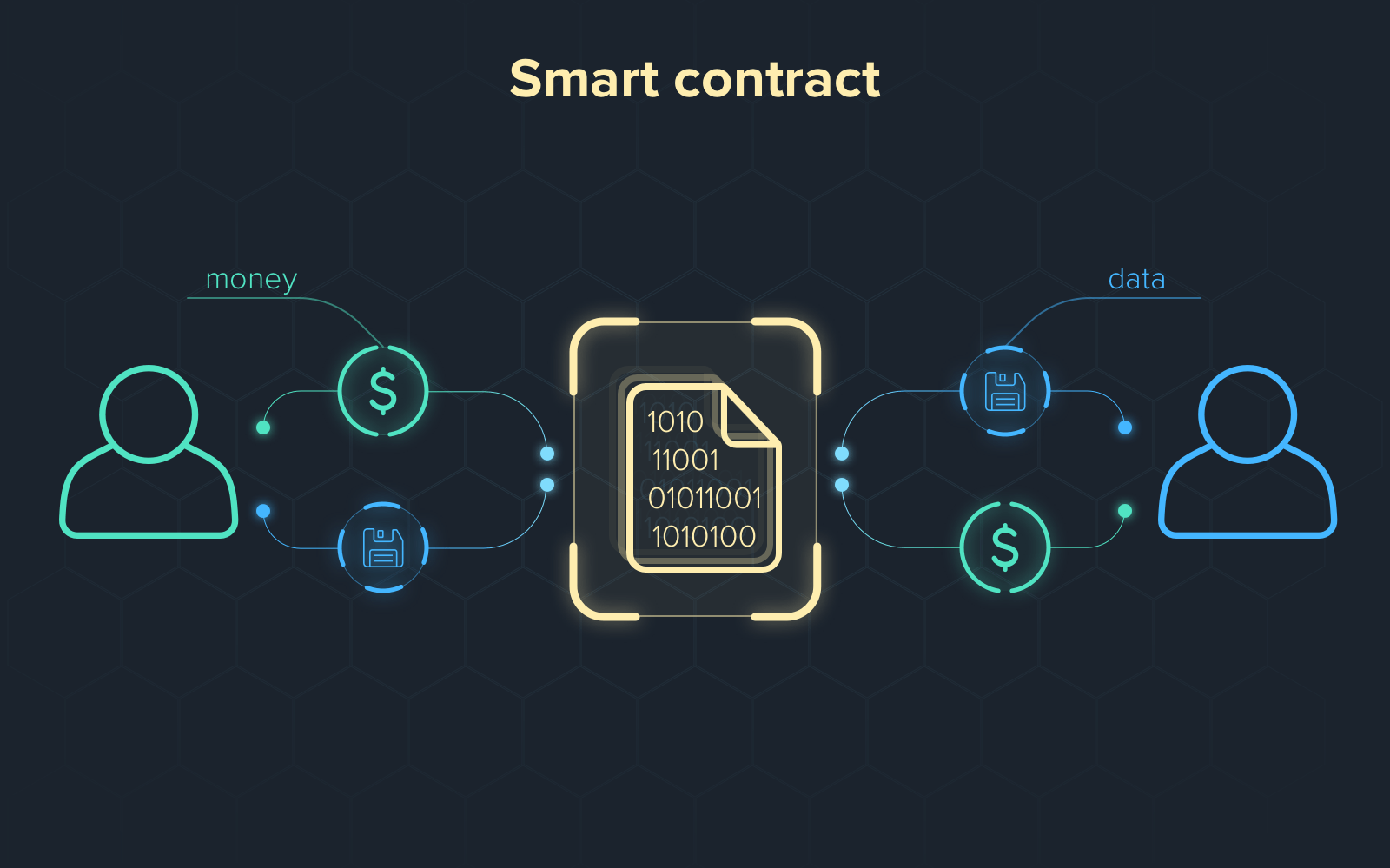

Smart Contracts

A smart contract is a computer code that can be added to the blockchain to help make, check, or negotiate a contract. Smart contracts work based on a set of rules that users agree to. When these conditions are met, the agreement’s terms are carried out automatically.

Assume a potential renter wishes to use a smart contract to rent an apartment. By paying the security deposit, a tenant gets the apartment’s door code. Both parties would send their agreements to the smart contract. After storing the door code and the security deposit, the smart contract would automatically exchange them on lease start. The smart contract will return the security deposit if the landlord does not provide the door code by the lease date. This eliminates the need for a notary, third-party mediator, or attorney, as well as their associated fees and procedures.

Supply Chains

As in the case of IBM Food Trust, suppliers can use blockchain to keep track of where the materials they buy come from. This would let companies check not only the authenticity of their own products but also the authenticity of common labels like “Organic,” “Local,” and “Fair Trade.”

Forbes says that the food industry is using blockchain more and more to track the path and safety of food all the way from the farm to the consumer.

Voting

As mentioned above, blockchain could be used to facilitate a modern voting system. Voting with blockchain carries the potential to eliminate election fraud and boost voter turnout, as was tested in the November 2018 midterm elections in West Virginia.5 Using blockchain in this way would make votes nearly impossible to tamper with. The blockchain protocol would also maintain transparency in the electoral process, reducing the personnel needed to conduct an election and providing officials with nearly instant results. This would eliminate the need for recounts or any real concern that fraud might threaten the election.

Pros and Cons of Blockchain

Even though it is hard to understand, blockchain has almost unlimited potential as a decentralized way to keep records. Blockchain technology could be used in ways other than those listed above, such as to give users more privacy and security, lower processing fees, and fewer mistakes. But there are also some disadvantages.

- Pro

Improved accuracy by taking people out of the verification process

Cost reductions by getting rid of third-party verification

Decentralization makes it harder to tamper with

Transactions are secure, private, and efficient

Transparent technology

Gives people in countries with unstable or underdeveloped governments an alternative to banking and a way to keep their personal information safe

- Cons

Bitcoin mining involves a lot of expensive technology.

Low transactions per second

History of being used for illegal activities, like on the dark web

Regulations vary by country and are still not clear

Data storage limitations

What Is a Blockchain Platform?

A blockchain platform lets users and developers make new ways to use a blockchain infrastructure that already exists. One example is Ethereum, which has a native cryptocurrency known as ether (ETH). But the Ethereum blockchain also lets people make smart contracts, programmable tokens that can be used in initial coin offerings (ICOs), and tokens that can’t be exchanged for cash (NFTs). All of these are built on top of Ethereum and kept safe by nodes on the Ethereum network.

How Many Blockchains Are There?

Every day, the number of live blockchains grows at an ever-faster rate. As of 2022, there are more than 10,000 active cryptocurrencies that are based on blockchain, with several hundred more non-crypto currency blockchains.

What’s the Difference Between a Private Blockchain and a Public Blockchain?

A public blockchain, which is also called an open or permissionless blockchain, is one that anyone can join and set up a node in. Because these blockchains are open, they need to be protected with cryptography and a consensus system like proof of work (PoW).

On the other hand, in a private or permissioned blockchain, each node must be approved before it can join. Since nodes are considered to be safe, the security layers don’t need to be as strong.

What’s Next for Blockchain?

Blockchain is finally getting a name for itself, and it’s not just because of bitcoin and other cryptocurrencies. The technology has already been put to use and is being researched for many real-world uses. Blockchain is a buzzword that every investor in the country is talking about. It has the potential to make business and government operations more accurate, secure, cheap, and efficient, with fewer middlemen.

As we get ready to enter the third decade of blockchain, it’s not a matter of if legacy companies will adopt the technology, but when. Today, there are a lot more NFTs, and assets are being turned into tokens. The next few decades will be an important time for blockchain to grow.